Last month, I sat across from a couple in their mid-50s who had done everything right. They maxed their 401(k) every year, lived below their means, and had accumulated just over $1.4 million in tax-deferred accounts. On paper, they looked like retirement success story. In reality, they were staring down a tax problem that was going to cost them hundreds of thousands of dollars if we did not act before 2026.

That conversation is happening in my office on repeat right now. And if you have a meaningful amount sitting in a traditional IRA or 401(k), it should be happening for you too.

Here is what I am telling every client who will listen: the window we have right now for Roth IRA strategy in 2026 and the years leading into it is genuinely one of the most significant planning opportunities I have seen in my 20 years in this business. The Tax Cuts and Jobs Act of 2017 expires after December 31, 2025. Unless Congress acts — and I would not count on that — we are looking at a near-automatic reversion to higher marginal rates starting January 1, 2026. What you do between now and then matters enormously.

What Changes in 2026 and Why It Matters for Your Roth Strategy

Let me be specific, because most blog posts gloss over this. Two corrections to how this was originally written. First, for tax year 2024 the figures of $47,150 (single) and $94,300 (married filing jointly) are the point at which the 22% bracket begins, not where it ends — the IRS states the 22% rate applies to incomes over those amounts (IRS tax year 2024 inflation adjustments). Second, the TCJA rate schedule did not sunset: the One Big Beautiful Bill Act (P.L. 119-21, signed July 4, 2025) made the individual rate brackets permanent, so 22% does not become 25%, 24% does not become 28%, and the top rate does not return to 39.6% in 2026.

That is not a rounding error. For someone sitting in the 24% bracket today, converting $100,000 from a traditional IRA to a Roth IRA costs $24,000 in federal taxes. That was the arithmetic while the 24% bracket was still scheduled to revert to 28% after 2025 — a $4,000 difference on the same conversion. That reversion never happened: the One Big Beautiful Bill Act made the TCJA rates permanent, so the 2025 deadline pressure described here no longer exists. Bracket management still matters when you size a conversion — the cliff does not.

The clients I am most concerned about are those in their late 40s through early 60s who have substantial pretax balances and are not yet drawing Social Security. That gap between retirement and Required Minimum Distributions — what we call the RMD window — is prime Roth conversion territory. You have lower income, lower tax exposure, and time for those converted dollars to grow tax-free.

The Specific Conversion Strategy I Am Running Right Now

For most of my eligible clients, I am recommending what I call a bracket-fill conversion approach. The goal is to identify how much income they can convert each year while staying at the top of their current bracket — without tipping into the next one. For a married couple with $80,000 in ordinary income, that means we may have room to convert another $14,000 or so before hitting the 22/24% bracket threshold.

This sounds simple, but the execution is where people stumble. You have to account for Social Security provisional income rules, Medicare IRMAA thresholds (which kick in when your MAGI exceeds $212,000 for married filers in 2025 — $206,000 was the 2024 threshold), capital gains harvesting plans, and state taxes. In my experience, the clients who just pick a round number and convert without modeling the full picture often end up overshooting in ways that trigger unexpected costs.

I run a full tax projection for every client before we execute a single conversion. If you are working on your own, tools like the Roth conversion modeling features inside tax software can help, but they require accurate inputs. Knowing your numbers — your actual monthly budget, spending, and income sources — is foundational.

What About the “Just Invest and Pay Taxes Later” Argument?

I hear this regularly: why pay taxes now when you do not know your future rate? It is a fair question and I want to be honest — there are situations where Roth conversions are not the right answer. If a client is currently in the 32% bracket or higher and expects to be in a lower bracket in retirement, aggressive conversion may not pencil out. Same if someone has significant deductions today that reduce their effective rate, or if they are planning to give heavily to charity through a Qualified Charitable Distribution strategy later in life.

The blanket advice to “always convert to Roth” is as oversimplified as “always maximize your 401(k).” Context matters. What I am saying is that for the majority of pre-retirees who are currently in the 22% or 24% bracket with sizable pretax balances, the math favors acting before 2026 — and acting with a plan.

Backdoor Roth and Mega Backdoor Roth: Still Worth Using

For higher-income clients who exceed the Roth IRA contribution limits — $161,000 for single filers and $240,000 for married filers in 2024 — the backdoor Roth IRA remains a valuable strategy. You contribute to a nondeductible traditional IRA and then convert it immediately to Roth. The key caveat is the pro-rata rule: if you have other traditional IRA balances, the conversion will be partially taxable. I have seen this catch people off guard more than almost any other planning mistake.

The mega backdoor Roth, which involves making after-tax contributions to a 401(k) and converting them in-plan or rolling them out, can allow up to an additional $46,000 or so in Roth contributions annually depending on plan limits and employer match. Not every employer plan allows this, but it is worth asking your HR department directly.

Getting Organized Is Not Optional

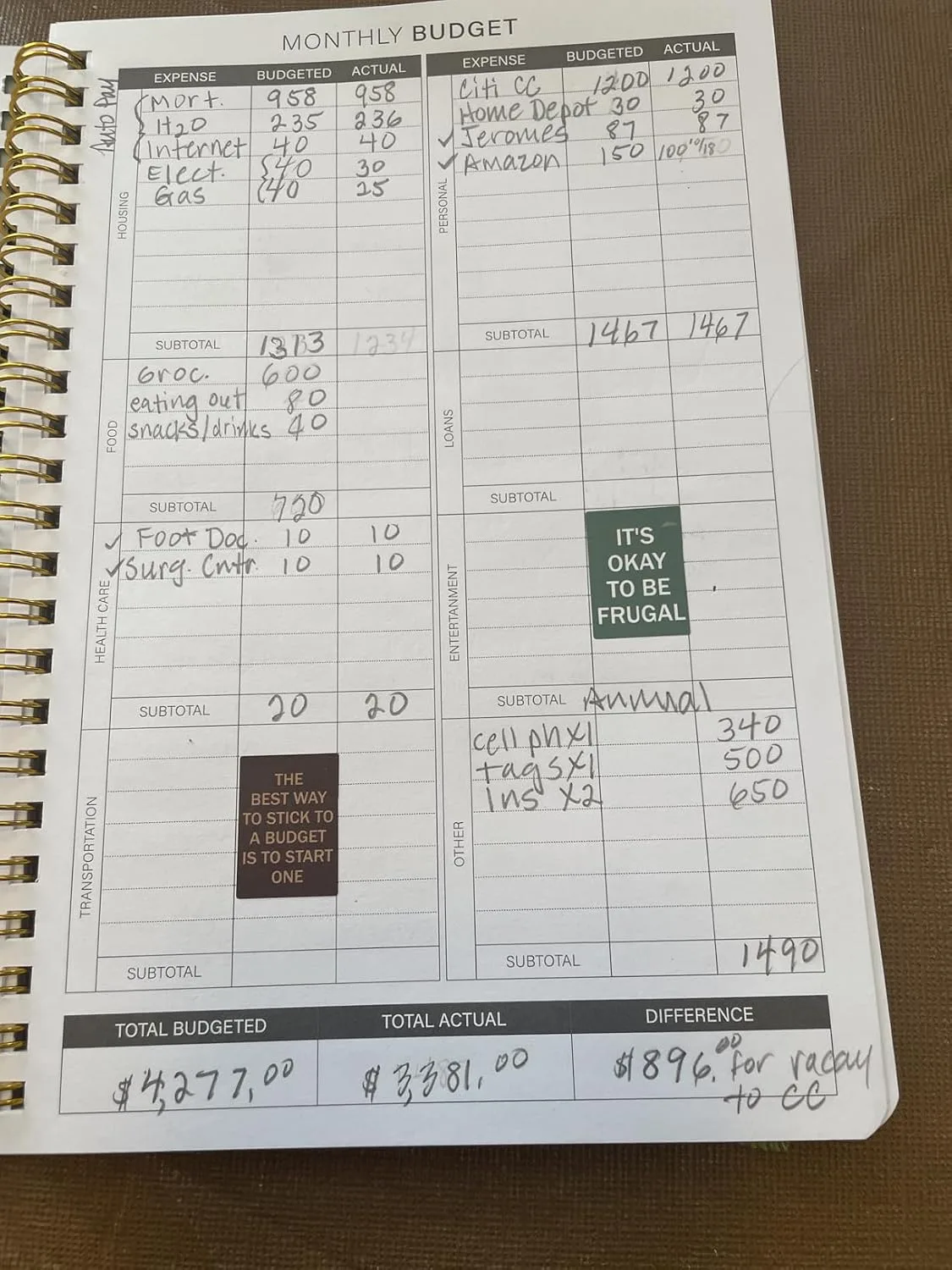

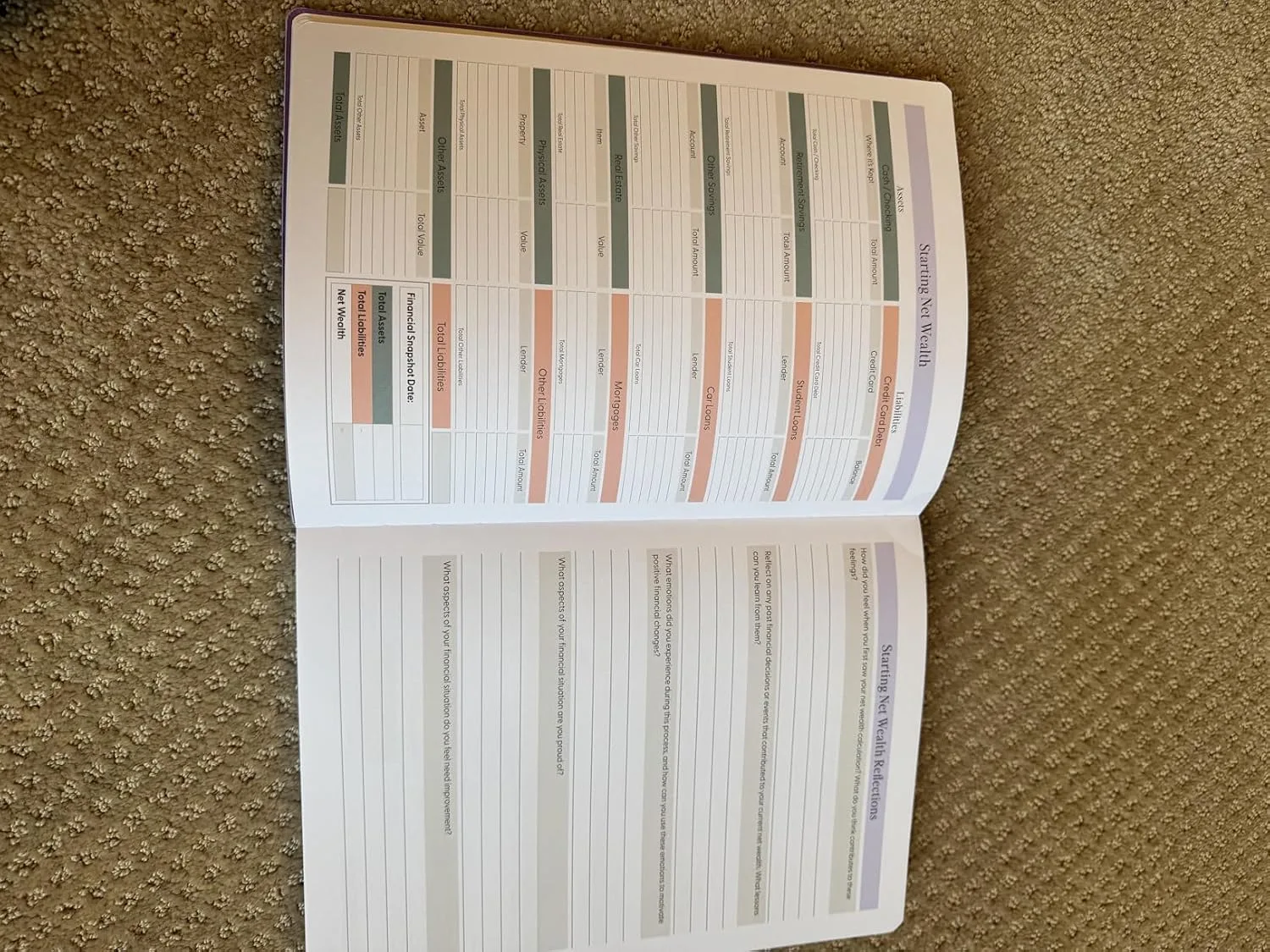

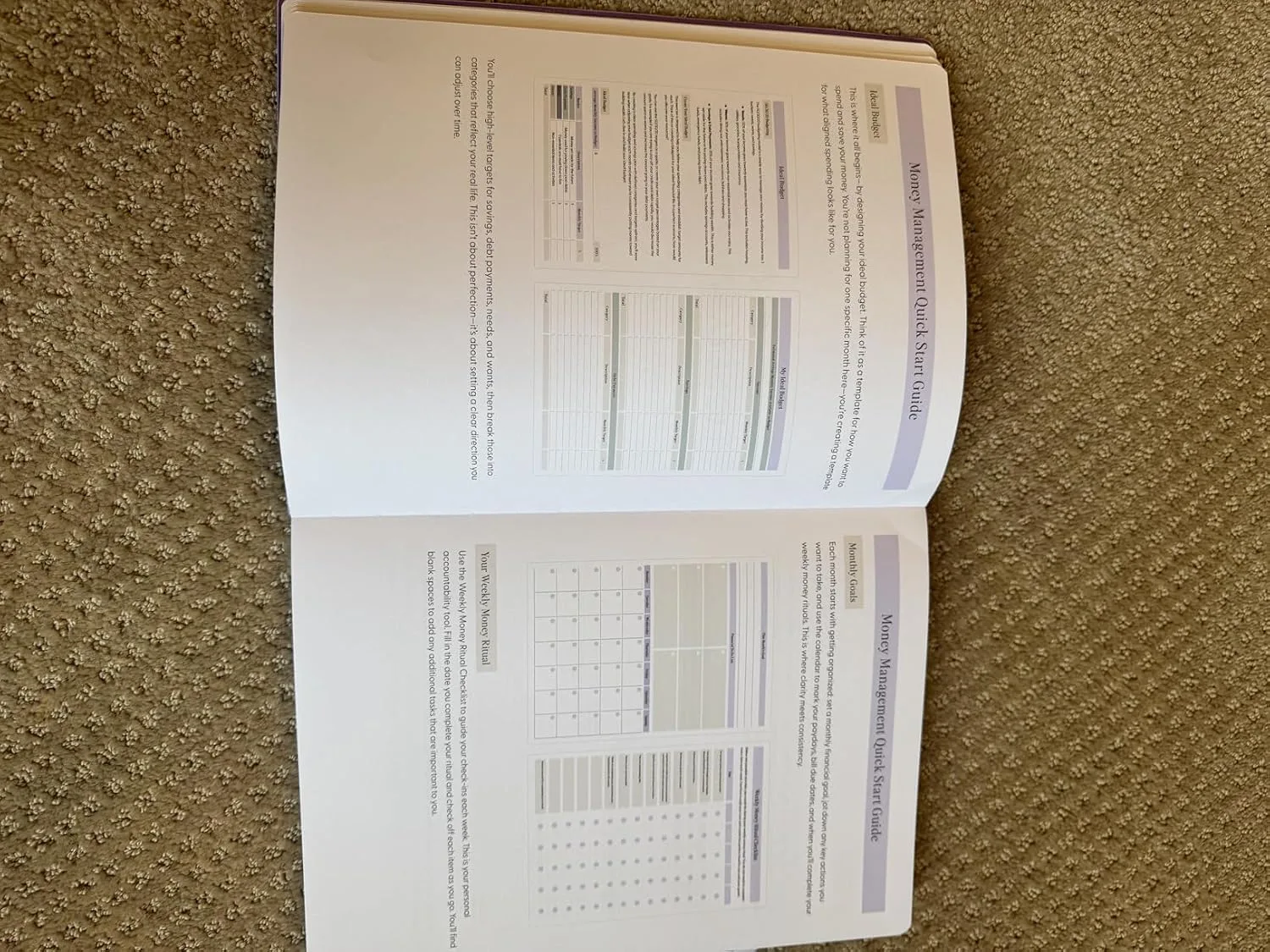

One thing I stress with every client is that tax-efficient retirement planning only works if your financial picture is clear and up to date. I have worked with people who genuinely did not know what they were spending each month, which makes it nearly impossible to model income needs, bracket exposure, or conversion amounts with any accuracy.

Getting your finances organized on paper — tracking income, fixed expenses, variable spending, and bill due dates — creates the foundation that makes every other strategy work better. It sounds basic, but the clients who have this handled are the ones who execute well.

This post contains affiliate links. As an Amazon Associate I earn from qualifying purchases.

What I Use and Recommend

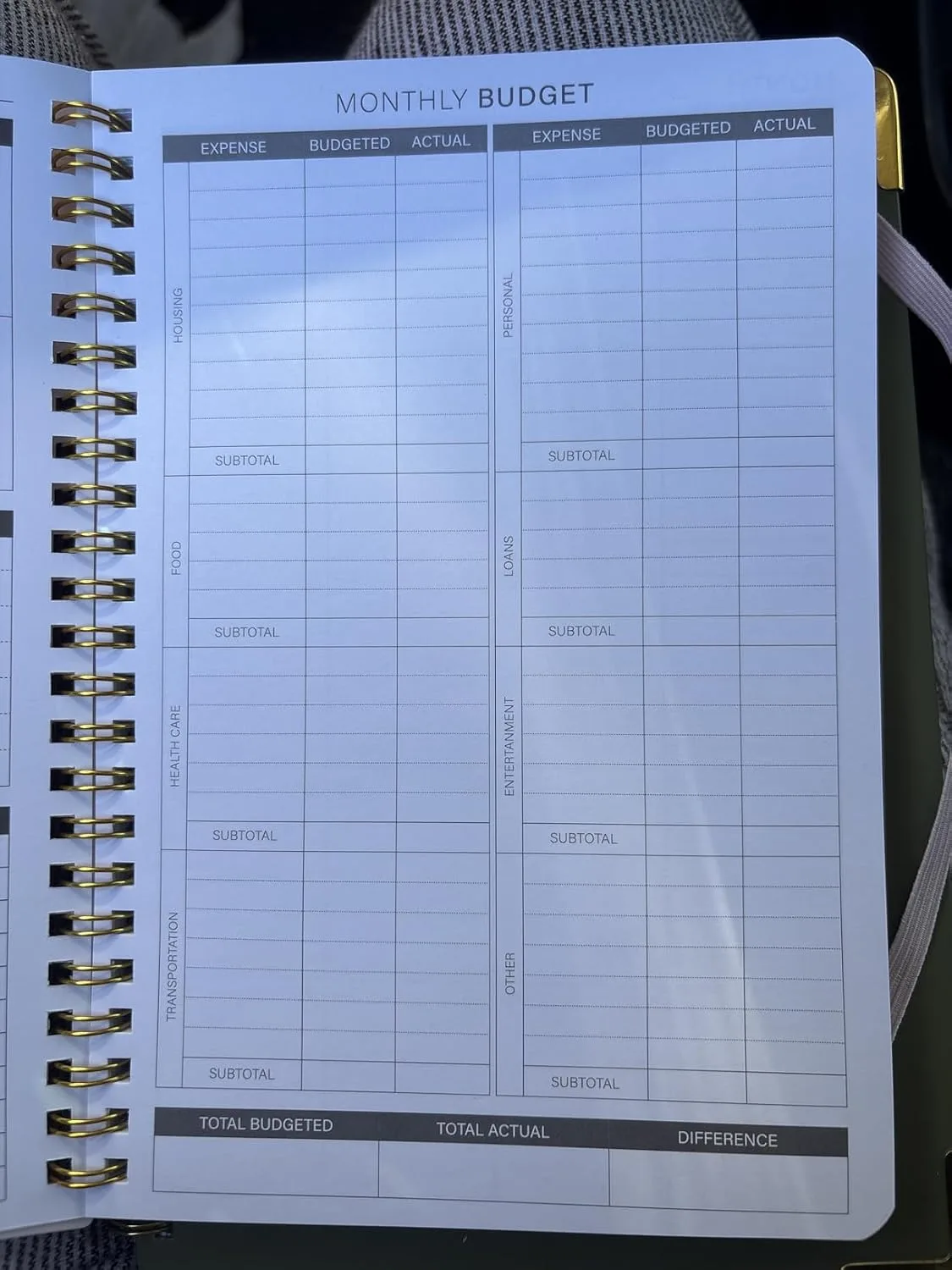

For clients who want a tangible way to get their financial picture organized, I often point them toward physical planners that make budgeting and expense tracking concrete. Two that I have recommended:

- Dow Janes Planner Panda Planner Budget Planner 2026 Financial Planner – Monthly Budget Planner & Bill Payment Tracker, Expense Tracker Notebook, Budget Book, 8.5 x 11 Softcover Purple 120gsm — a well-structured annual planner that works well for mapping out income and expenses month by month, which is exactly what you need when planning conversion amounts.

- Budget Planner – Monthly Budget Book with Expense Tracker Notebook, A5 Monthly Financial Organizer Planner, Manage Your Money Effectively, Start Anytime, 1 Year Use, Green — a compact, flexible option that does not require a calendar year start, which makes it practical if you are beginning your planning mid-year.

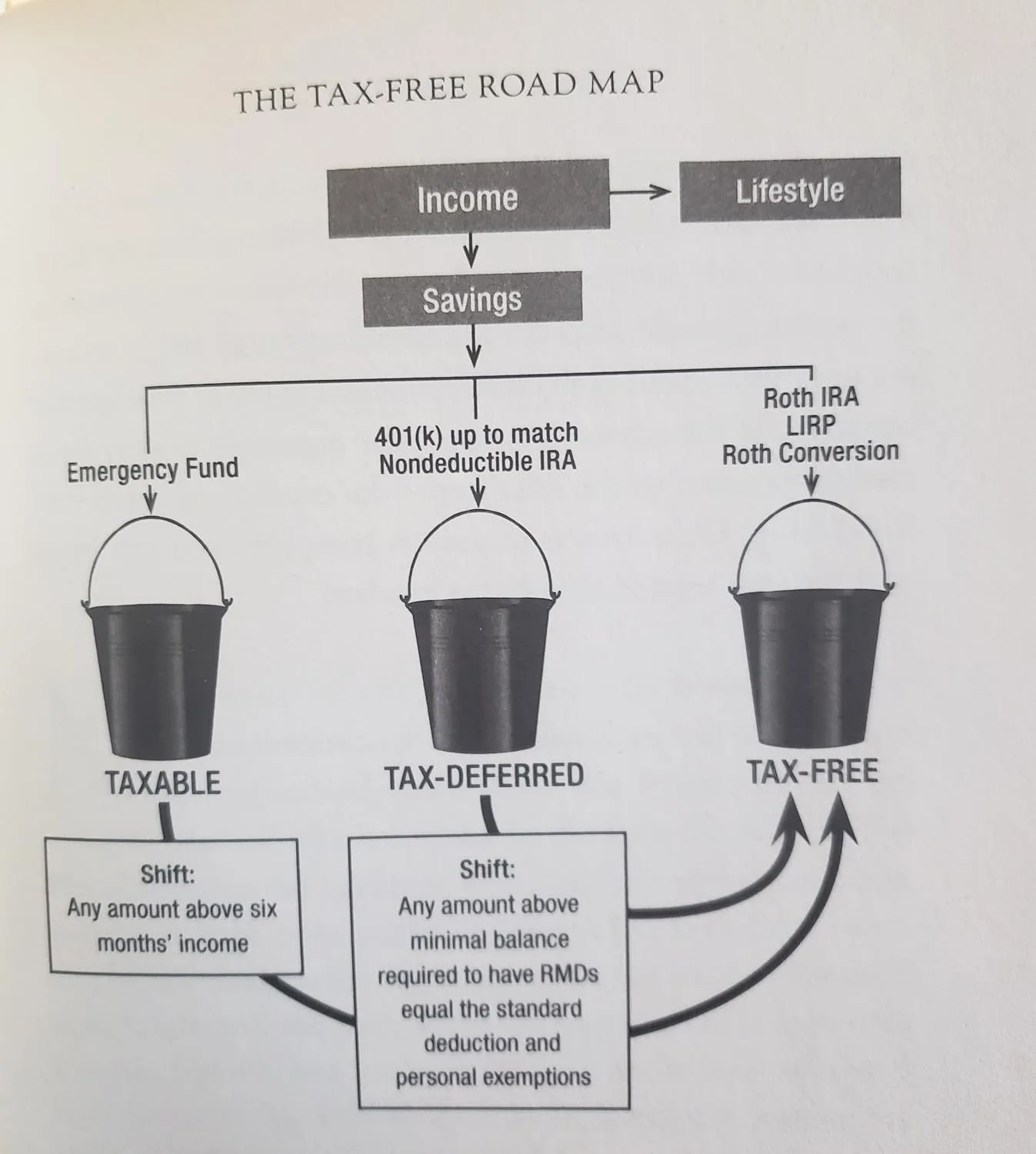

On the educational side, one book I consistently recommend to clients who want to understand the strategic logic behind Roth conversions and tax bracket management is The Power of Zero, Revised and Updated: How to Get to the 0% Tax Bracket and Transform Your Retirement by David McKnight. I do not agree with every position in the book, but it articulates the long-term logic of tax diversification clearly and is accessible for non-financial professionals. It has started many productive planning conversations with my clients.

The Bottom Line

The TCJA sunset is not a rumor or a hypothetical. It is current law. Your Roth IRA strategy for 2026 and beyond needs to account for a likely shift to higher tax rates, and the planning window is shrinking. For most people with meaningful pretax retirement balances and current income in the middle brackets, the next 12 to 18 months represent a genuine, time-sensitive opportunity.

Work with a fee-only advisor to model your specific numbers. Get your budget and income picture organized so you have something real to work with. And do not assume that what made sense three years ago still makes sense in the current landscape. Tax law changed once. It is about to change again. The question is whether your strategy changes with it.

The Book That Made Me Stop Treating Roth Conversions as “Nice to Have”

If you’re sitting on a large tax-deferred balance like my mid-50s clients were, you need a framework for thinking about tax brackets and lifetime tax exposure—not just year-to-year moves. This book gave me the language and strategy to actually model what “zero tax” means in retirement and why waiting until RMDs hit could be catastrophic.

What works

- Forces you to think in decades, not tax years—suddenly the urgency of converting before 2026 clicks because you see the full cascade of future RMDs and bracket creep

- Gives concrete scenarios for people with $1M+ in tax-deferred accounts, which is exactly the group that gets blindsided by conversion math they never learned

- The revised edition reflects updated rules, so you’re not reading around outdated SECURE Act assumptions or old thinking

What doesn’t

- It’s strategic framework, not a tax return—you’ll still need a CPA or planner to actually execute the conversions and model your specific numbers

- Dense enough that if you’re looking for a quick read about Roth basics, this goes deeper than you might want

I’ll admit: the first time I read it, I thought it was overstating the risk for people with moderate balances. Then I started seeing it play out in client after client conversation, and I realized I’d been underestimating the power of tax drag across a 30-year retirement. If you’re advising others—or managing your own seven-figure tax-deferred money—grab The Power of Zero, Revised and Updated: How to Get to the 0% Tax Bracket and Transform Your Retirement and actually sit with the math.

This post contains affiliate links. As an Amazon Associate, I earn from qualifying purchases at no extra cost to you.

The Power of Zero, Revised and Updated: How to Get to

I reference this book when clients finally understand why their conversion math starts in year one, not at 70½.

Check Price on Amazon →